14 / 144

14 / 144

13

Frontken Corporation Berhad (651020-T)

ANNUAL REPORT

2016

Financial

Review

(cont’d)

The consolidated net profit attributable to shareholders of the Company for FYE2016 was RM20.0 million, an increase of

RM16.0 million or 400% compared to the net profit attributable to shareholders of RM4.0 million for the preceding financial

year was mainly due to better performances by our non-wholly owned subsidiary. This translated to basic earnings per share

in FYE2016 of 1.91 sen compared to basic earnings per share of 0.39 sen in the previous financial year.

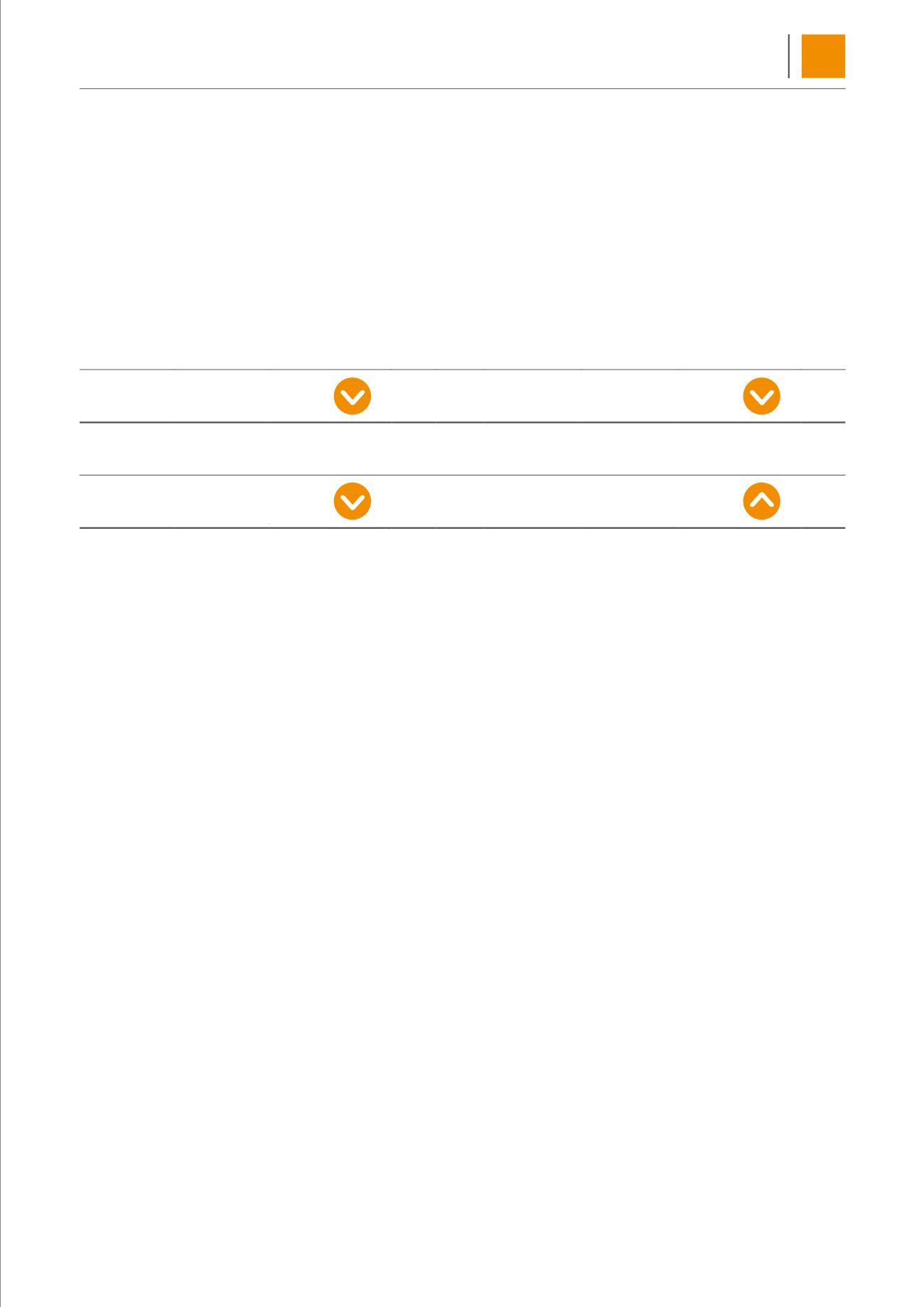

CASH FLOWS

in RM’000

NET DEBT

WORKING CAPITAL

2015

(66,482)

2%

2015

130,727

0.4%

2016

(65,287)

2016

130,255

FREE CASH FLOW

CAPITAL EXPENDITURE

2015

37,381

55%

2015

7,197

288%

2016

16,882

2016

27,901

The free cash flow reduced from RM37.4 million to RM16.9 million in FYE2016 mainly due to higher capital expenditure in

relation to the plant expansion of our subsidiary in Taiwan compared to the preceding financial year.

The net cash from operating activities was RM44.4 million and RM44.5 million in year 2016 and 2015 respectively. The net

cash inflow from financing activities of RM6.2 million in year 2015 as compared to net cash outflow for financing activities

of RM18.5 million in year 2016 was resulted from issuance of shares in year 2015 following conversion of the warrants and

higher loan repayment in year 2016.

Net cash used for investing activities increased from RM7.4 million in the preceding financial year to RM35.0 million in year

2016. The increase in cash outflow for investing activities was mainly due to higher capital expenditure, investment in cash

management fund and lower withdrawal of fixed deposits in year 2016.

Our Group has cash and cash equivalents of RM98.1 million as at the end of year 2016 compared to RM105.1 million at the

end of year 2015. The Group will continue to exercise prudence in cash flow management while conserving the cash for

potential future expansion and investing activities.

FINANCIAL POSITION

The Group’s shareholders’ fund improved from RM236.6 million as at 31 December 2015 to RM261.6 million as at 31

December 2016 due to increase in retained earnings.

Total assets of the Group increased from RM389.9 million as at 31 December 2015 to RM407.8 million as at 31 December

2016. Total Group’s liabilities of RM112.4 million as at 31 December 2016 were lower by RM6.2 million or 5% compared to

the previous year. The Group’s borrowings decreased from RM43.3 million in year 2015 to RM29.3 million in year 2016 due

to the repayment of borrowings via Group’s surplus fund during the financial year.

The total Group’s borrowings as at 31 December 2016 that is repayable within one year is 30%. Singapore Dollar borrowings

represented 37% of the total borrowings whilst borrowings denominated in Taiwan Dollars and Ringgit Malaysia made up

48% and 15% of the total borrowings respectively. Foreign currency borrowings were drawn to hedge against our Group’s

overseas investments and receivables which were denominated in foreign currencies.